Iscriviti alla Newsletter

per continuare a costruire le tue finanze, un passo alla volta. Capire cosa sta succedendo sui mercati non serve a prevedere il futuro, ma a prendere decisioni più consapevoli.

Ludovic Phalippou, the Oxford professor who has spent twenty years dismantling private equity myths, is finally a guest on The Bull. The verdict is clear: private equity is a "billionaire factory", not because it generates extraordinary returns for investors, but because astronomical fees, misleading metrics and brilliant marketing have made fund managers fabulously wealthy, not the people who put up the money.

312. Debunking the myths of Private Equity and Private Credit with Ludovic Phalippou

Private equity is a billionaire factory, not a return factory

IRR is not a rate of return: it's a misleading measure

Illiquidity premium: the mechanism doesn't exist in private equity

Volatility laundering: apparent low volatility, hidden real risk

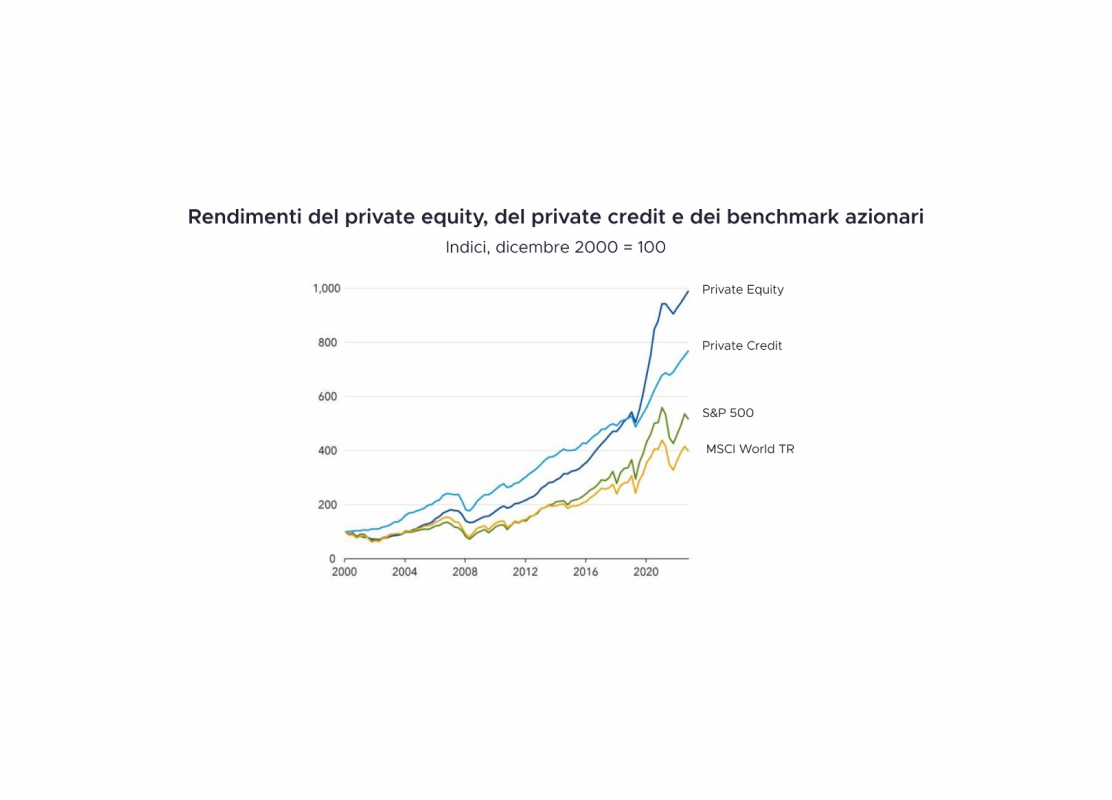

Apollo's real returns: about 11% over 5 years, not 39%

"Democratization" is marketing, not fair access to better opportunities

ELTIFs: watch out for fees, unverifiable NAV and so far low returns

Final advice: diversification, low fees, optimize your tax situation

Ovunque ti trovi, non correre rischi: proteggi la tua privacy.

Goditi streaming e download senza rallentamenti e accedi ai tuoi contenuti preferiti anche quando sei all’estero.

Approfitta dell’offerta esclusiva dedicata agli ascoltatori di The Bull!

Riccardo

Welcome to my podcast, The Bull.

Ludovic Phalippou

Thank you for having me.

Riccardo

Professor, you have become one of the most uncomfortable voices in private markets fields and possibly the most authoritative voice in academia as far as private markets are concerned. I know that some large firms have somewhat pushed back against some of your research about topics concerning private markets. What made you decide this was a fight worth taking?

Ludovic Phalippou

There was nothing special or particularly interesting. I was doing a PhD and I had to find a topic. Someone had some data, I worked with them, and that’s how it went. There’s nothing personal and I’m not particularly passionate about the topic, which I think is a good thing. I think people should be careful about studying things they are passionate about because then they will bring in quite a lot of biases.

Riccardo

Yeah.

Ludovic Phalippou

I have no bad experience or anything that triggered any kind of passion or hate. I just analyze data and write what I see.

Riccardo

Through analyzing data you have come up with a lot of myths concerning private markets. I feel that telling the truth was disturbing for the industry.

Ludovic Phalippou

Yeah. I mean it’s an industry that is very good at producing bullshit, like most industries. You have a lot of misleading marketing and there’s a lot of money at stake. So that probably explains why there is more of it here. And I’ve seen it as my role as an academic, like in other fields, to debunk them, to explain what reality is and to bring the nuances.

Riccardo

Could you please tell us what you mean when you said private equity is a billionaire factory?

Ludovic Phalippou

A billionaire factory because they have minted a lot of billionaires and multi-millionaires. There are about 100 billionaires who were born not with any wealth, but with hardly any wealth and they have become billionaires thanks to a career in private equity as a private equity fund manager. And you have thousands of people who have accumulated 50, 100 million just being a fund manager. So there’s this billionaire factory image because a lot of billionaires have been minted by that industry, which is not a very big industry. And if you think they became billionaires because they are investment geniuses, that’s not what the data are showing. So that’s the thing, right? You have this factory of billionaires because, not quite out of nothing but out of nothing extraordinary, a lot of people were minted billionaires and multi-millionaires for sure.

Riccardo

It seems like the industry business model is much better than its product.

Ludovic Phalippou

Yeah. I mean, it’s not unusual in finance: it’s like you want to run the casino rather than being the guy playing. So yeah, the guys who have constructed the casinos, they got to, you know, it was clever in a sense. You charge these massive fees. People cannot even see exactly what you charge. You can play with the numbers so that your track records always look good, almost most of the time look good. So yeah and so people keep on sending you money and you charge extraordinary amounts and nobody really realized and you continue like this. So it’s yeah, more money has been printed for fund managers here practically than ever in hedge funds or in mutual funds or in any other type of finance.

Riccardo

Okay. Let’s start with one of the biggest elephants in the room which is the so-called liquidity premium. Basically, the old idea behind investing in private assets, going back to the infamous Yale model, is that if I lock up money for a very long time I should be earning a premium in excess of the public markets return. The whole storytelling seems compelling but in my understanding you’re skeptical about the existence at all of a liquidity premium.

Ludovic Phalippou

Yeah, it’s an expression that gets a lot of confusion. So, you’re basically saying — I’ll paraphrase it to make it more tangible — you’re saying there is a product which is quite crappy in terms of features. It is illiquid. I cannot get out when I want and it’s risky and so it’s got to give me a high return because otherwise why would anybody buy this, right? So, I’m going to buy this product because it’s going to give me high returns. So that’s it. So I designed a very crappy product, really unattractive, and then it will give me high returns because it’s so crappy. I mean, it’s weird, right? So like you said, because there is illiquidity and inconvenience of investing in these things, it should give me a higher return on average. But ‘should’ is not ‘will’, right? And through which mechanism would you get that? It’s very weird that people say, ‘Look, I have a product here, it’s really inconvenient. It’s really annoying. So it’s got to give me high returns.’ And so I’m buying it because I want high returns. Okay.

Riccardo

It’s a label for ‘please don’t ask too many questions for the next 10 years’.

Ludovic Phalippou

Yeah. Yeah. Yeah. It’s a myth. It’s part of bullshit that I’ve demonstrated. By now we know it was bullshit. It’s clear — there’s consensus — if anyone looked into it they understand now that they never had high returns in private equity. They used a measure of performance which is highly misleading. They were backed by Harvard Business School that made a case study with them and so on. And so the these guys, everybody was citing a written number for them but that never existed. They never accumulated wealth. So it’s pure fantasy and it’s clear by now. It’s been shown by me and I think widely accepted now. So we cannot use this argument anymore. Now the story that there can be an equity premium is natural, it’s Economics 101. But I can give you examples of where there would be an equity premium and we have a clear story for why. For example, with traded bonds: some are less liquid than others. The bonds that are less liquid have a higher yield, because otherwise nobody would buy the less liquid bond and so their price goes down until the yield is much higher for the liquid bonds and people say ‘okay at that price I can have it.’ If you want to buy a piece of real estate in my hometown in the middle of nowhere in France the yield on real estate unlevered is 10%. If you buy the same piece of real estate in Paris, it’s 3%. In London, it’s 3%. Why is that? Because I can sell that building or apartment in two weeks in Paris or London. And in my hometown, you may need two years to sell it if ever. So of course when people see that they say, if I’m buying this building to buy-to-let, I’m going to have to price it at an implied yield of 10%. And it would be 3% in Paris or London because much more liquid. There’s no such mechanism in private equity. What does it mean that you have taken some companies, you put them in an envelope and you say you cannot touch it and then by some miracle you’re going to get higher returns? I can get any stocks, I put them into something that doesn’t trade and then you get a higher return. Why? How? I can make a basket — I put 10 shares of Apple, 10 shares of Microsoft and I say you Ricardo can never trade this and you’re going to get an equity premium — how? There’s no mechanism. So there’s a lot of confusion around this terminology and the logic of it. Related to this point is the idea that people have that ‘oh but in the past it has outperformed public markets’. So that’s not quite true but it has performed all right in the past so far. But that does not mean it’s an illiquidity premium. You can just have a sort of investment that has managed to outperform another type of investment. The question is always — is it because you’re comparing two things that are not comparable? There’s always the one guy who’s going to perform better than the other guy. I don’t know, maybe we can take an Italian football parallel — what is the team in Italy that would have the highest number of titles in the first league?

Riccardo

Juventus.

Ludovic Phalippou

Juventus. So is there a Juventus premium? Like what does it really mean? One team has to be number one, right? Each year one team is going to win. It doesn’t mean this team has a premium of sorts. Simply, there’s got to be a winner. So if you say I’m comparing public equity and private equity, it’s two different strategies. Well, one of them will be higher and the other one lower, right? And it happened that — if you exclude the last few years because we don’t quite know what the prices really are — in the 2000s and 2010s private equity was very different in Europe and the US. But in the US it was probably 1% at best above public equity if you are comparing comparable things. And in Europe it was more of a spread but it’s very hard because it’s completely different what they typically invest into and what public equity is. The point is: it could have been the other way around. One type of investment will always be above the other.

Riccardo

Thank you. As far as the word ‘return’ is concerned, a moment of enlightenment for me was when I read a piece you wrote for the Financial Times, debunking the whole idea of the internal rate of return as a measure of performance in private equity and private credit. Private equity firms tend to say that their IRR has been very high for a very long time as a proof of their consistency over time in delivering great results and you have been brutal about it for good reason. Why is IRR such a misleading metric when it comes to private assets, especially when compared with a compound growth rate of return for example of the S&P 500, which is the typical benchmark?

Ludovic Phalippou

Because it’s a fantasy measure. It doesn’t measure rates of return. It’s like expected goals in football — it’s as if the team will say ‘I had 50 goals last year’ and then it’s written ‘expected goals’. I’m not lying, I had 50 expected goals last year, sure, but they’re not goals — we need to know goals. It’s the same with internal rate of return: a rate of return cannot be calculated in private equity, so people invented something, making some assumptions and coming up with something that looks like it. But the advantage of that is because it’s a bit clunky, I also know how to cook it so that this number looks high as well, and then I present it like this. People who know, know it’s BS; people who don’t know believe it, and you get attention. That’s what happened. Even nowadays people use IRR as if it is a rate of return, but it has nothing to do with a rate of return. The correlation with an actual return is meaningful only in a certain range; outside of that, it’s pretty much uncorrelated.

Riccardo

Yeah. When Apollo says their return since inception is 39%. What does it mean?

Ludovic Phalippou

Nothing. It has nothing to do with how much people earn in Apollo. I mean it’s easy: you just look at the accounts of Apollo. All their fund performance is there in their filings, publicly available. You go to the 10K filings for all their funds and you will see that on average their funds return about 1.6 times the money. So you gave them $1, they gave you back $1.6. Now the key question is how long did it take? Usually it’s about five years. So that means you got about an 11% return.

Riccardo

So that’s pretty close to that of the public stock market.

Ludovic Phalippou

And then basically the stock market.

Riccardo

Another trick is to pick the right benchmark to magnify your performance and this is a common practice in private markets.

Ludovic Phalippou

Yeah. So you have all these indices that are out there in the nature and you take the one with the lowest return so that you can beat it. It’s as simple as this. And again, it wouldn’t be so sad — people throw money thinking these guys are geniuses. And so that’s what I’m talking about when I say bullshit marketing: they think they’re geniuses, throwing money at these guys, and these guys charge massive amounts of money and become billionaires or semi-billionaires because they played around with benchmarks and slides. I mean, really.

Riccardo

Okay. Another myth, which seems also very compelling for great institutional investors, is that private assets are somewhat less volatile than the public equivalent and uncorrelated, which is probably due to the fact that they are not marked to market every day.

Ludovic Phalippou

I invest in wine. I have a lot of wine in my cellar. I can ensure you that the volatility is zero and I’m not correlated with public market. So there’s no problem. I can do that, because I value the wine myself every year and it goes up by 5% every year because I decided so. It’s fine. As far as the UK is concerned, we value the farms ourselves. We have zero volatility. We value our funds every year. Then we come up with whatever number we want to come up with and we increase it by about 2-3% a year. Zero warranty, zero correlation with markets. Sure, you don’t need to pay fees for that. You can do it yourself.

Riccardo

Yeah. What’s the reason behind the race toward private assets? For example, now if you are an institutional investor or you run a great pension fund, you have a sizable amount of assets under management invested in private markets, under the idea that you are better diversified that way. I suppose asset managers are smart and they understand all this stuff.

Ludovic Phalippou

That’s unprovable. You can be as smart as you want — you cannot prove it. You can bring whoever you want as an expert, but how do you prove diversification? And we know another result: with 20-30 well-chosen stocks you’re already sufficiently diversified. So what does it mean? It’s not because you add something different to your portfolio that you are more diversified. If you have well-chosen stocks spread across geographies and industries, it’s pretty hard to say that private equity would add diversification. Now, intuitively, you could say that if you have, for example, private equity in tech in Europe, you could say that because there aren’t many European tech stocks, it probably brings something you don’t have in your portfolio. But again, it may be that the correlation is super high anyway, so it doesn’t matter that you’re missing that sector because it correlates with other things in Europe. Maybe you could make that argument — if you do venture capital in China in your portfolio, that brings you something you’re not exposed to. In those cases, you could maybe make that argument. But if you say you’re investing in a large buyout US fund, you look at the portfolio of these funds: it’s the same as the companies that are publicly listed.

Riccardo

Yeah.

Ludovic Phalippou

What diversification… and again, you could say ‘oh but they’re different things’. Sure, everything is different but they’re 99% correlated. What moves the value of equity in the US is very common forces, like war and things like that. And so you can say ‘oh but they have different names’. Yeah, but they go down if there is a war, they go back up if there is a war — not because they have different names, but because they react to the same factors. So, you need to be diversified to have diversification and be immune to volatility. But you can be diversified pretty quickly with 30-50 different exposures. You don’t need thousands and thousands. I believe in diversification. I don’t believe that institutions really do it for diversification — there are papers that show that consultants play a big role in this. The consultants have an agenda because they make more money advising expensive products.

Riccardo

Sure.

Ludovic Phalippou

For people it’s also a lot more fun to invest in something interesting than not, and you know, people are humans — they don’t want to be bored at work. So if at work people tell you ‘do you want to invest in government bonds?’ you’re like ‘what the hell, it’s boring, it’s like math.’ And then they say ‘do you want to do equity?’ — sometimes you can invest in football, in Formula 1, you can invest in football clubs, you can invest in all kinds of exciting things. Yeah, it’s a lot more interesting.

Riccardo

So it’s not a fundamental reason.

Ludovic Phalippou

And of course, people would generate these graphs saying ‘oh but the returns are even better’. So everything is better, they tell you to do it. The returns, there are some papers that say they are good. It’s more exciting. It has no volatility. It’s fantastic.

Riccardo

Yeah. The maybe fastest growing segment in the last 10 years is private credit and for years it was sold as a safer, more disciplined, more resilient way to invest in corporate debt. What did most investors get wrong about private credit during the boom while now we are seeing why they were wrong?

Ludovic Phalippou

So I’m not sure we are seeing now they were wrong, but in the different cycles of this market — in 2016 and 2018 I was skeptical about private credit because what was effectively happening is that private credit was going pretty low in the capital structure, very junior, and in particular the American ones were levering up their debt. So it’s again back to the label thing: you can label something debt, but if you borrow money — like you borrow yourself 100 at the bank, you put 100 of your own money, you lend 200 to a company covering 60-70% of the capital structure — you can call it debt if you want, but there’s a lot of what we would call equity risk here. Each tranche has a different risk profile. You can say ‘oh but it’s a fixed payment that I put in place, so it’s debt.’ Sure. But if you have one chance in ten to be repaid, then it’s as if you had equity. So there was this ‘search for yield’, right? But with private debt: ‘I get 10%, I can give you a 10% coupon, no problem. I can say: if Microsoft generates more than one trillion in profits, you will have a 10% coupon.’ The problem is you have one chance in a million to get it. But I can write a contract saying ‘I will pay you 10% coupon if the following thing happens’, which will hardly ever happen. So there was a manufacturing of high yield by having things that are super risky, and therefore they had high yield, but what matters is not the yield. The yield is the maximum you can earn on a debt instrument. What you care about is the expected return, which is the yield times the probability that you get that money. So when interest rates were zero, the main issue with private credit was the manufacturing of yield by producing extremely risky instruments that still had the label ‘debt’ but were effectively equity risk. And now there is research by other people showing that indeed there is quite a lot of equity risk in these private credit funds. Then came the interest rate increase, where people said ‘oh my God, we’re practically toast because with this increasing interest rate our companies that are so highly levered will never manage to repay all this debt.’ But how about private credit? We also sell private credit and this is cool because now with the interest rate increase you make 12%. And people are like ‘oh my God, this is so cool, here’s all my money.’ But the 12% is because of the increase in interest rates — you charge 12%, but how many people are going to take that at 12% in a high interest rate environment where the economy is not doing very well? So my second wave of criticism of private credit in that period was that the train had left the station: you will not make 12% and your money won’t be easily deployed at 12%. I haven’t tracked that; I doubt they deployed much money at 12%. It’s not easy to track. And now they have a third, new problem coming up — which was to be anticipated — which is that the companies have to pay 12%, they don’t have the money, they cannot repay all this debt, so they kind of postpone things. And because private credit doesn’t want to say ‘my company is bankrupt,’ they say ‘no, it’s not bankrupt, I’m just postponing when they will pay me back.’ So we all carry on. It’s tricky because then we don’t believe their net asset values, we don’t believe their marks. And in a closed-end fund, it doesn’t matter if I don’t believe your mark. If you’re an open fund, it’s a different matter.

Riccardo

Do you think that we are discovering in these weeks, with all the turmoil going on in the private credit industry, that the model was built for a zero rate environment that no longer exists and that cannot be sustainable in a higher for longer ecosystem?

Ludovic Phalippou

No, I don’t think this was a problem. I think fundamentally private credit can exist in any environment. It can be higher interest rates. The leverage private credit — yes. Levered private credit is easier in a zero interest rate environment. When there’s a higher interest rate, you don’t lever up. But private credit in itself — the idea that it’s not a bank doing the loans but a fund, and they call the money whenever they have a loan to make — makes complete sense. This is much more sensible than banks. Okay. So it makes total sense. Fundamentally, private credit makes sense. The levered private credit is very risky, and that was the issue I had with that, and investors were not fully aware of that, I don’t think. And then there’s this idea that when interest rates went up they would just deploy at 12% — I thought it was also fantasy and misleading. But fundamentally private credit has a role to play; they are very natural lenders, much more than banks, so they should be the lenders for almost everything. Now, when people are talking about the current crisis — there’s a bit of a crisis because they don’t collect the coupons the way they should and they are postponing some bad news and things like that — but it doesn’t seem to be the end of the world. It’s not going well, but it’s not the end of the world. Private credit by construction is quite resilient because they can renegotiate, postpone, take the equity they have to. So it’s designed in a pretty robust way. And we see the economy has not been doing well for many years. The interest rates went up a while back. There’s no catastrophe. Everything is fine. It’s just that you have 10% of that market where people went a bit bananas and decided to do open-end structures with credit, and you should just never have open-end structures with any illiquid asset, whether it’s credit or real estate and the like. And people have done that. I’ve said that for 25 years — I tell all my students that whenever we study fund structures and do exercises, we very quickly understand that if it’s illiquid, you don’t put it in an open fund, you put it in a closed-end fund. They are designed for that. But some people like open-end structures because they make more money, so they launched all these open-end structures, which are not appropriate for credit. And they are paying the consequences now: people are trying to get out, they can’t, people panic, there’s a bit of a run on the funds, and so on. But that’s just 10% of the credit market.

Riccardo

Okay, you don’t see systemic risks at this moment? The parallel with 2008 is very common.

Ludovic Phalippou

No. I testified at the UK parliament on this, and I had done similar things for the ECB etc. It’s been a long time that people are obsessing about the systemic risk of credit. What we see right now is just a run on a small part of the segment, which was vulnerable to a run by definition because it was not well constructed, the structure was not appropriate. I think there could be problems with insurance companies regarding how much they invest in private credit — that I think would be a problem. But as I told the parliament, it’s going to be a consumer protection issue. People are going to be very shocked when their life insurance company is bankrupt and so they won’t get the life insurance they paid for. That will cause a lot of disappointment and anger, but it’s not a systemic risk. It’s not a panic. It’s not like freezing the economy — that I don’t say.

Riccardo

Despite the meaningful exposure of some banks in financing the deals?

Ludovic Phalippou

Yeah. So indirectly some banks are exposed to private credit and also private equity, so if a bank went quite wild maybe that bank will go under, but yeah I don’t see it — I cannot imagine banks collapsing on this.

Riccardo

Okay. One of the great themes in the last three to four years is the ‘democratization of private assets’. The idea is to allow normal people to invest in very high performing assets once only allowed to high net worth individuals and institutional investors.

Ludovic Phalippou

It’s a brilliant story, again it’s a masterclass in bullshit. You take a name, like ‘democratization’ — who’s against democratization? Raise your hand. But is it democratization? No, it’s allowing everyone to invest in something they don’t understand. What does this have to do with democratization?

Riccardo

Yeah. What’s the real reason behind this?

Ludovic Phalippou

The real reason is to make money, right? So you say ‘I’m going to open up to more people so that I can make more money’. Okay. So that’s it. And then you say ‘I need to find a cool name so that people are on board.’ So I’m going to call it democratization. Wow, everybody’s in favor. But is it really democratization? No. It means allowing anyone to invest in something they don’t understand. It’s exactly what it is. You say ‘anybody is going to be allowed to buy cannabis’ — or even better, do it with cocaine. Only rich people have had access to cocaine. It’s very unfair, right? So I want the government to provide cocaine to everyone to control the prices so that everybody can buy cocaine. I’m going to call that the democratization of cocaine. Brilliant. So it’s exactly what it is, right? And so you say ‘Okay, so democratization — it was only for the rich.’ Wow. And so now you can do it. Oh, cool. Now even the rich didn’t really understand the product. They signed things they didn’t understand. And so now you don’t understand the product either. But yeah, you can be screwed like the rich people were before. Great. That’s great progress. And so you allow these people who have no clue about the product to invest in what you said are high-performing vehicles. They are not. Of course, if you think an IRR is a rate of return, you think it’s high performing, but they are not. But it’s really, really a masterclass in bullshit. Brilliant. You choose the words so that people think it’s a noble thing. You then give performance metrics that people won’t understand and think are high. You completely hide all the fees they will be paying. You have 200 pages of terms and conditions that people won’t read and will give you the money anyway. You don’t even read the iTunes terms and conditions, and there are few pages in private equity — when you buy private equity funds there are 200 pages of terms and conditions but absolutely nobody reads them. In fact, you don’t even have access to them. And you call that democratization. So okay, you have a product, there are 200 pages of terms and conditions with all kinds of weird, wild things in there, you don’t even get to read them, but sign here and you’ll be like a rich guy with access to the same things. It’s great. It’s amazing.

Riccardo

Yeah. I’m afraid about the final questions because in Europe we now have the ELTIF 2.0 and they’re being presented as a way for ordinary investors to access long-term opportunities and better diversification. And I’m also skeptical about investing in private assets because when you buy an ETF you know what you’re buying. When you buy a vehicle which invests in private companies it’s very hard to figure out what you’re actually doing. But anyway, these products are being pushed and more people will be questioning if they should have ELTIFs in their portfolio for better diversification, higher returns or whatsoever. What do you think they should be thinking about before taking this decision?

Ludovic Phalippou

Do they understand the product? Do you know what’s in it? Have you read the terms and conditions? Have you ever read the limited partnership agreement? Do you know it’s 200 pages? Are you able to read that and understand what’s in there? Do you understand that an internal rate of return has nothing to do with the rate at which your wealth will accumulate, etc., etc.? And the returns of these products so far that I’ve seen are very low. But maybe it’s because they’re too new, or I don’t know, but they don’t seem very high. And on top of that, you need to trust the NAV. But even if you do, the returns I’ve seen are not particularly high. That being said, there’s nothing wrong with investing in private assets. I think public markets are not particularly useful or making sense — people don’t need to trade every millisecond and so on. So the most natural way to invest is in a private asset. In fact, most people invest in real estate for example, which is a private asset.

Riccardo

Yeah.

Ludovic Phalippou

The problem is when you have massive rules for anybody who proposes a product on public markets and there are no rules if you propose a private asset. In Europe you have more rules than in the US; in the US there are some rules but they are very mild. So you can still have people showing misleading return numbers, lying about the fees or presenting fees in a misleading manner. You allow all this misleading stuff. There’s nothing wrong with private assets. I think private markets make a lot more sense than public markets, but you need to have the same or similar level of rules, disclosure, comparability, information. You can call it sophistication, but knowledge — that’s not there.

Riccardo

Is it something that must remain a niche and not a wide industry? Because in the 1980s and ’90s, maybe when David Swensen started to invest in private equity, it could have made sense for that specific time, at those specific fees, in that specific environment.

Ludovic Phalippou

They didn’t make any extraordinary amount of money in private equity.

Riccardo

Okay.

Ludovic Phalippou

In the 1990s when you went into venture capital they had good returns, but not every venture capital fund did well. In the 1990s they were investing in growth companies, and if you had invested in the NASDAQ you would also have had high returns. So all he did was start investing in venture capital in the 1990s when he became CIO, and he had good returns in the 1990s investing in growth stuff, just like anyone. Okay, maybe he had more return than others, but we don’t have data to prove that one way or the other. We know the return of the endowment from 2000 onwards: 11%, which is good, but it’s the market. So there’s no ‘oh it was good for Swensen but no longer works’ — like we hear these stories. They are just myths. People like these myths; it’s exciting, like betting on horses or on football. People like to debate: ‘I know this guy, he always gets the right score’, or like the octopus during the World Cup that chose the right team all the time and became a superstar. We need to be careful about these tendencies.

Riccardo

Thank you. Last question. 95% of my guests are American. So when I ask them to please give me one piece of advice if they were to give advice to a 30 year old about how she should invest for the long term, they are typically biased toward buying an index fund or an ETF that tracks the broad stock market and staying put. You are French, you work in the UK and you have a very good understanding of the US environment. So I would like to have your point of view, which is more of a mixed one instead of the typical American one. The practical question is: how would you suggest to invest?

Ludovic Phalippou

What you said is what any investment textbook would say, so that’s the usual advice. If you’re lazy, you say: ‘Okay, if I don’t know anything about you, then just do this — at least it won’t go very wrong: buy a few low cost, well-diversified vehicles you can access with low cost, and then just do that.’ Okay, so that’s the easy one. When I advise family offices and people who can really invest — and again, a lot of people think they can invest. If you have 10,000-100,000, you cannot really invest. First optimize your mortgage, make sure you have no credit card debt, no student debt — under 100,000, don’t think about it too much. But if you have more than one million of liquid wealth, then we can start talking. So what I say to my clients is we work throughout — including taxes — and be very clear on the different products’ tax implications: some have particular tax advantages. To illustrate quickly: my college endowment — I’m on the investment committee — we are tax exempt because we’re a charity. In the UK if you buy any real estate you have quite a large stamp duty, like 5%, and then some other taxes. We pay none of that. So if we’re going to buy a pub, we get it at 5% less cost than anyone else — a natural advantage. That’s why we have a lot of real estate in the UK in my college context. As an individual, I should not do real estate in the UK. In the UK there is the ISA, the equivalent of the 401k in the US but more generous: you can invest up to about 25,000 euros a year tax-free in a certain number of eligible products — broadly speaking, publicly listed instruments. You can have one for your children, 9,000 a year, one for your spouse, another 25,000 a year, etc. So in the UK you can go tax-free within listed markets and if you have a good ISA provider buying the products will be pretty cheap, and you could deploy up to around 70-80,000 euros a year in these products. That’s it. That’s how you should do it, because nothing will ever beat the tax advantage — the tax advantage is so massive that your genius in investing and choosing investments will not beat your tax savings. Very important — you have to think of the fees you pay, because you can always be more diversified but if I want to buy Indonesian real estate, yes it diversifies, but the problem is I don’t know anything about it and to find the right person and execute the transaction will cost me a fortune, so I should not do Indonesian real estate. The fees you pay are very important. And then I spend a lot of time thinking about the objective — where are you going to spend your money, in which currency, what is the money for? It’s linked to your lifestyle. What is it you want and what are the main risks in your life? So that you can think of hedges. For example, if you work in the oil industry in the UK, having quite a lot of exposure to China is actually pretty smart because the Chinese economy tends to be negatively correlated with oil, and your career depends on oil doing well. So you probably don’t want to have shares in Saudi Arabia and Norway. Depending on your job and source of income, there are natural hedges for you — that’s how I construct portfolios. That’s not very often explained in textbooks; very few people do it. It’s a long answer, a very tailored answer. But the lazy one is: just buy diversified portfolios, low fees, all good.

Riccardo

Thank you for the lazy and the not-so-lazy answer because it was one of the most interesting I’ve heard here. Professor Phalippou, thank you so much for being here. It was a remarkable conversation and thank you for what you do for the field. I also suggest anyone to read whatever you put on LinkedIn because it’s always fun. It’s not easy to talk about finance and be fun at the same time. Thank you so much for the service you provide.

Ludovic Phalippou

Thank you very much.

Ludovic Phalippou, il professore di Oxford che ha passato vent'anni a smontare i miti del private equity, è finalmente ospite di The Bull. Il verdetto è netto: il private equity è una "fabbrica di mil...

Il private credit è diventato in pochi anni una delle asset class più discusse e ambite, capace di promettere rendimenti elevati e una stabilità apparente che sembra quasi troppo bella per essere vera...

In questo episodio, insieme a James Choi, parliamo dell’importantissimo ruolo delle azioni in portafoglio, della formula di Merton e di quelli che sono alcuni esperimenti mentali che possiamo adottare...

Negli ultimi anni molti grandi investitori istituzionali stanno cambiando il modo di costruire i portafogli. Il classico modello 60/40 tra azioni e obbligazioni potrebbe non essere più sufficiente....

In questo episodio di The Bull facciamo un bilancio concreto del 2025 partendo dal mio portafoglio, ma soprattutto da una distinzione fondamentale che ogni investitore dovrebbe conoscere: la differenz...

Il Private Equity sta occupando sempre più spazio nei portafogli istituzionali e stanno aumentando le opportunità di investimento anche per i privati. In cosa consiste? Quali sono i rischi e le opport...

Quando capisci come funziona la finanza… ti viene voglia di raccontarla!

Da quando l'ho scoperto in 15 gg mi sono ascoltato 150 puntate senza fermarmi, ho annullato gli altri podcast per portarmi alla pari ed ascoltare tutte le precedenti puntate, ben fatto, esattamente il livello di informazione che mi serviva

Gianluca G., 11 Set 2025Non sono solito a mettere recensioni e specialmente non ascolto podcast, ma da quando ho iniziato questo, faccio fatica a staccarmi, e quasi non posso più fare a meno di ascoltare e arricchirmi culturalmente.

Andrea V., 22 Set 2025Podcast piacevole, scorre veloce ma in modo estremamente chiaro, spiega i concetti chiave per gestire le proprie finanze, fornendo la classica cassetta degli attrezzi. Complimenti, davvero ben fatto!

Massimiliano, 29 Mag 2024Riccardo mi ha letteralmente cambiato la vita e fatto scoprire che amo la finanza, ho ascoltato il podcast già due volte e non mi stufo mai di ascoltarlo, parla in modo semplice e chiaro

Massimo D., 23 Set 2025Veramente interessante, chiaro e conciso. Cambia la vita finanziaria di chiunque.. da ascoltare assolutamente anche per chi di finanza non vuole occuparsi mai

Francesca B., 6 Apr 2024Podcast che dà sempre spunti interessanti che personalmente mi ha fatto appassionare alla finanza personale spingendomi ad approfondire in prima persona.

Lorenzo, 13 Mar 2025La mia ignoranza in materia mi ha sempre creato dei dubbi, ma grazie a un amico ho iniziato ad ascoltare il podcast. Per fortuna che ho 24 anni e un po' di tempo e soldi da dedicarmi a imparare le varie nozioni per me stesso. Grazie mille!

Luca G. 10 Ott 2025Ho acquistato e letto il suo libro e l' ho trovato. Esprime i concetti economici in modo semplice e chiaro. Sentirlo parlare conferma che è un professionista del settore.

Giulia N., 11 Ago 2025Dovrebbero ascoltarlo buona parte degli italiani e io avrei dovuto scoprirlo con qualche anno in anticipo ma meglio tardi che mai

Matteo C., 3 Set 2025